The CFTC Is Regulating Event Markets Alone. We Filed Five Proposals to Help.

And, the exam that licenses prediction market professionals has ZERO questions about prediction markets.

The CFTC has the large task of regulating the new $64 billion asset class with no self-regulatory organization backing it up, no dedicated exam standard, and no standardized data infrastructure across platforms. The CFTC is the lone Marshal of the new west that are prediction markets. We’ve filed a formal public comment on the record to the CFTC on ways we think can improve markets for traders, operators, and the public.

On March 16, the CFTC published an Advance Notice of Proposed Rulemaking on prediction markets (RIN 3038-AF65).

Prediction markets traded $64 billion in notional volume last year. The asset class has a dedicated lobbying apparatus, mainstream media coverage, and pricing data that gets cited by foreign governments.

The comment period is open. Any member of the public can submit a comment on the federal record.

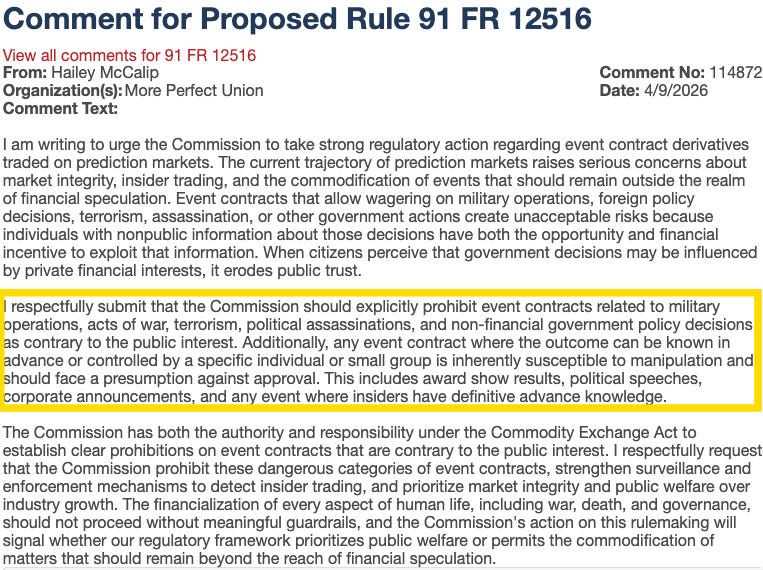

Sadly, most comments are boiler plate blogs of text about how Prediction Markets are bad, evil, and scary. They’re devoid of any rational argument, and are rooted in feelings not fact; and there are dozens of copy and pasted comments like the one below. They use scary terms like terrorism, and war; in an attempt to sell a narrative that Kalshi traders are running around betting on coups and bloodshed.

Except, they aren’t.

They can’t.

Because these type of contracts are already prohibited under the law.

In an attempt to provide some more color beyond individuals spamming the public record with copy pasta. Today, we submitted a formal public comment raising five issues we believe no other commenter has raised in the docket. The full comment is linked at the end of the article. This is the short version

What we propose

1. A prediction market Self Regulatory Organization (SRO.)

Every other regulated asset class in the U.S. has at least one self-regulatory organization between the exchange and the federal regulator. Equities have FINRA. Municipal bonds have the MSRB. Prediction markets have nothing. The NFA has no jurisdiction over exchanges — only over intermediaries like FCMs

The CFTC is supervising this entire asset class alone, directly, with no buffer. We proposed a structurally independent PM-SRO, modeled on the precedents Congress set when it created the MSRB in 1975 and consolidated FINRA in 2007. A prediction market only SRO would allow disputes to be resolved outside of Kalshi’s current format of dispute resolution. We believe this would stand to benefit traders greatly.

And a point we think is one of the most important:

The current professional exam which governs event contracts (Series 3) contains zero questions about event contracts.

Event contracts are very nuanced, settlement mechanics, listing, disputes and other variables can be confusing and highly technical. A registered commodity professional can pass the Series 3 and know nothing testable about the fastest-growing product class on CFTC-regulated exchanges. So we proposed a dedicated “Series PM” competency exam.

This is like if the bar exam covered every area of law except criminal defense, but passing it still licensed you to represent murder defendants. The courthouses are full. The caseload is exploding. And every public defender walking in the door passed a test that never once asked them what “beyond a reasonable doubt” means.

2. Prohibit branding between registered and unregistered platforms.

At least one operator runs a CFTC-registered domestic platform and an unregulated offshore platform under the same core brand name. In early 2026, a contract on the death or removal of the Supreme Leader of Iran resolved differently across these two platforms. Same brand. Different outcomes. The domestic platform cancelled the contract. The offshore platform paid out. We proposed mandatory branding separation, point-of-sale disclosure, and a prohibition on cross-platform promotion of unregistered affiliates.

Dual branding of regulated + unregulated platforms confuses the general public, especially with markets relating to events which are banned under the CEA.

3. Mandatory algorithmic trading disclosure.

The whole policy argument for prediction markets is that prices reflect distributed human judgment. That argument falls apart if an undisclosed share of volume comes from bots running arbitrage and market-making strategies. We proposed a framework modeled on the CFTC’s own previously proposed Regulation AT: registration of automated trading systems, monthly publication of aggregate automated-volume statistics, and strategy-category disclosure. No proprietary parameters exposed. Just enough transparency to know whether the “wisdom of crowds” is actually a crowd.

“Penny Jumping” is a popular bot tactic on Prediction Markets.

A bot sees a bid at $0.55 and an offer at $0.58, posts $0.56 and $0.57, and captures the penny spread on both sides without any opinion about whether the event will happen. The price on screen looks like a probability estimate. It's actually two algorithms fighting over a penny.

4. Standardized public API and data reporting.

Prediction market prices show up in news broadcasts, policy briefings, and intelligence assessments. No two registered platforms publish data in the same format. You can’t do cross-platform surveillance if every exchange speaks a different data language. We proposed a standardized public API, five-year historical archives, and daily automated surveillance reports — analogous to the Consolidated Audit Trail for equities. If this data is going to be treated as public information infrastructure, it should meet a public information standard.

Why we filed

First Strike Research is a financial research operation. We trade prediction markets. We study them. We’ve built tools to analyze them. We have a direct commercial interest in these markets functioning with integrity, and a direct analytical interest in their data being accessible and standardized.

We also think the CFTC is at an inflection point. The Commission asked the public for input. Most of the comments in this docket, from what we’ve seen, argue about whether prediction markets should exist or how wide the product scope should be. Those are fine questions. But the plumbing questions — who watches the exchanges, what data standards apply, how do you tell bots from humans in the order book — are where the actual regulatory failures are happening right now. That’s what our comment addresses.

Read the full comment

Our complete comment, in PDF Format, with legal citations and proposed remedies for each section, is linked here.

First Strike Research

outreach@firststrike.trading