Will the real AI company please stand up?

Our research shows this little known broadcaster has a robust AI engine poised to drive growth

In a market where shoe companies are pretending to be AI companies, the real AI companies tend to be the ones you least suspect.

Disclaimer: The author of this article is ‘long’ and owns shares in the company covered. The author stands to benefit from any rise in the share price and may sell, or close this position at any time. This is not investment advice. Please read our terms of service

In this case, Entravision — EVC 0.00%↑ — is misclassified by the market as a legacy Spanish broadcaster. While, yes, technically they are in-fact a legacy broadcaster which is merely, in our opinion, their margin of safety behind their booming mobile ad-platform; which generated 154 million in Q1-2026, and equated to an impressive +204% year-over-year. The company’s legacy media assets provide stability, but the investment case is increasingly driven by its fast-growing digital advertising platform. Their digital advertising platform is built on a proprietary AI system which we believe is still grossly undervalued by the market.

But first, you must understand why EVC is an AI platform, that happens to be in legacy broadcasting—

A machine learning titan before the AI boom.

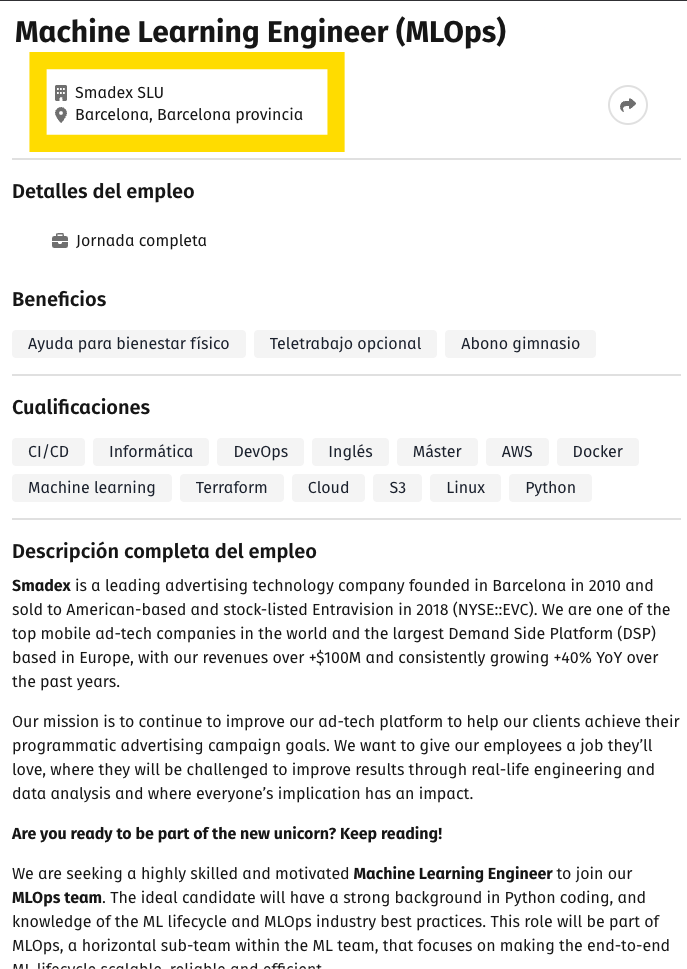

EVC acquired Smadex in 2018, and built a machine learning (a/k/a AI) advertising platform well before the boom of AI chatbots like GPT and Claude.

EVC owns Smadex and Adwake which are the core to EVC’s Advertising Technology and Services (ATS) segment. Combined, they generated 270 million in full year 2025 revenue, and then proceeded to nearly match that number in Q12026 alone.

It is very important for investors to understand what Smadex and Adwake does as they both represent the diamond in the rough the broader market has overlooked in a fever dream over AI-chatbots.

Smadex is a mobile device centric demand side platform (advertising.) It’s software that functions as the brain that sits on the advertiser side of the digital ad auction market. Smadex in real time computes calculations for millions of ad slots across mobile apps, and then predicts which users are most likely to do what (install, purchase, register etc.) and Smadex places bids automatically. At the core is a robust, proprietary machine learning engineered trained to predict the future of a user (which sounds a-lot like we do, but with earnings calls.)

Adwake on the other side of the coin is the managed services and growth layer built on top of Smadex. Where Smadex is the plane, Adwake is the pilot, navigator, and flight-crew. Adwake runs advertising campaigns for clients across gaming, fintech, e-commerce etc.

We can not stress enough, that the combination of Smadex and Adwake forms a fully organic Machine Learning-AI (ML-AI) company hidden inside a broadcaster. There is still tremendous upside for this stock that the market still has not priced in.

Truly organic AI companies are RARE.

Most self described “AI-Companies’ are in-fact, not AI companies. They’re AI wrappers, they consume tokens, and pass queries to the likes of Anthropic and OpenAI. Which makes them no different than a toll booth built on rented land. The toll booth operator owns NO property, and anyone can do it.

EVC, is in a very unique position, because they own the land, they own the toll both, and are the sole benefactor of a system they developed that is truly proprietary.

LLM inference costs account for 80-90% of total on-going cost of using AI, and is one of the largest margin strains for AI-Companies. The problem starts to snowball with their rate of revenue. Which in turn compresses margins and reduces operational leverage. In short, for the toll-both operator, the rent’s going up.

BUT—EVC doesn’t have this problem.

Because Smadex is the polar opposite of this: according to their own published engineering documentation, Smadex processes one million bid requests per second, each requiring a complete AI-driven bidding decision within a 100-millisecond window. At that latency requirement, an external API call is physically impossible — the round-trip network latency alone would consume a meaningful fraction of the entire budget. Every inference is executed internally, on proprietary models, on infrastructure that Smadex controls

Smadex’s in-house ML models are performing several simultaneous computations:

Conversion probability prediction: What is the likelihood this user, in this context, will complete the target action (install, purchase, registration)?

Bid price optimization: Given predicted value, what is the optimal bid that maximizes expected return rather than just win rate?

Budget pacing: How should this bid interact with campaign pacing, frequency caps, and daily budget constraints?

Creative selection: Which ad format and creative is most likely to drive the desired outcome for this specific user?

All of this is running on their own, proprietary deep learning models that Smadex’s in-house ML team trains.

The key insight for all of this is: Smadex (EVC) does not outsource anything. There is no OpenAI API Call, there is no per-hit cost to a third party inference vendor. The cost of running this is embedded into Smadex’s cloud infrastructure via AWS. Even if you own the land, and the toll booth, you still have to pay the power company.

If we look at a similar company running something equivalent on a non-native stack even at generously discounted enterprise rates; we watch margin health rapidly deteriorate. Smadex and EVC do not have this problem. Because Smadex was built from the ground up. EVC owns the land, and EVC owns the toll booth (Smadex, Adwake)

Agentic Margins

We reviewed a Smadex Machine Learning Engineer job posting and can deduce management is fully aligned with using Agentic-AI as a high fulcrum growth lever. Most companies, eat into their margin health with run away AI spending in an attempt to keep up with the times. EVC will not have this problem, because machine learning and advanced neural networking is the core of their business.

Special Forces soldiers are often referred to as ‘force-multipliers.’ In a holistic sense, we view agentic engineering teams in a similar lens as they produce more output per headcount than traditional engineering teams. Independent benchmarks from enterprise deployments in 2026 show that agentic coding tools reduce software development costs by 20–45% and deliver a code review agent completing a routine pull request for $0.72 versus $48 of senior engineer time — a 66x cost reduction on standardized work.

Applying this directly to Smadex: their engineering headcount is being hired specifically to build and maintain automated ML systems. Each hire is effectively operating at a multiplied output rate compared to a traditional engineer. Management noted in the Q1 2026 call that they "invested in our engineering team to continue to improve our technology and build more powerful AI capabilities into our platform" and simultaneously increased operating leverage. The two facts are connected: the agentic architecture of their engineering team means that adding engineers does not add engineering costs proportionally — because each engineer is running ML pipelines that automate large portions of their own workflow.

We believe ATS revenue will comfortably outpace ATS engineering costs over the next three years, which in turn will improve margin health—because the team is building a system that compounds their own productivity and they are doing it with an already professional coded, purpose built, in-house system. Most companies are building their AI-car as they drive it. But EVC built the car 5 years ago, and now all management has to do is a drop-in upgrade.

What Is EVC Actually Worth?

We are not applying aggressive assumptions to get there. We are not extrapolating the 204% growth rate forward indefinitely. We are simply asking: what would a standalone, profitable, ML-native programmatic DSP doing $650+ million in annual revenue trade for if the market knew what it was looking at?

The answer is: not $7.

Based on ATS segment economics, with 154.6 million in Q1 revenue and 23.3 million 34.3 million in operating profit as our base, we applied a conservative ad-tech EBIT multiple discounted relative to a comparable public company AppLovin ( APP 0.00%↑ )

We come to a base case conservative price target of $12.00

We say conservative because in this model we are modeling the legacy broadcast business (FCC Spectrum, Political Advertising) at ZERO.

For now, this is enough for you to understand why EVC may not look like an AI-forward, and efficient DSP on the surface, but it shows the deeper you dig into the company. And the market still has only scratched the surface for this stock.

EVC shareholders had a preview of what happens when the market starts pricing EVC like the ML powerhouse it actually is instead of the sleepy broadcaster it appears to be on the surface.

In our next EVC post we’ll cover our Bear/Base/Bull scenarios and map ATS operating profit more specifically.

Credits

A special thanks to The Value Road for setting the foundational coverage for this stock on Substack. I’ve been long the stock based on their analysis going back to late 2024. You can read his coverage here:

Disclaimer: The author of this article is ‘long’ and owns shares in the company covered. The author stands to benefit from any rise in the share price and may sell, or close this position at any time. Nothing in this article is investment advice.